Temporary Closure Due to the coronavirus restrictions, many businesses are having to temporarily close and allow staff to help sustain operations via home working. We wanted to give you some general advice about how to protect your premises during any temporary closures. This guidance is from a risk management perspective. Please give us a call should you have any queries relating to insurance cover.

Risk Control Measures:

Waste: Remove all external waste, pallets and empty skips ahead of closing.

Waste bins: Empty all waste bins and relocate to a secure area, ideally at least 10 metres from the building. If this is not possible and bins and skips are within 10m, these should have lockable lids.

Fire Systems: Ensure that any fire and/or sprinkler systems are fully operational

Fire Doors: Carry out a check to ensure that internal fire doors are closed

Building Utilities: Shutdown any non-essential electrical devices and building utilities. Isolate nonessential services, gas valves etc.

Inspections: Where at all possible (and subject to Government restrictions) try to implement periodic inspections of the building (internally and externally). Please ensure that you comply with existing government guidance regarding vulnerable people and lone worker risk assessments. Consider the provisioning for alternative skilled personnel, such as security guarding/patrolling companies.

Physical Security: Carry out a check to ensure physical security measures are in place e.g. fences are in good repair, windows are locked, shutters are in place, gates are locked.

Intruder Alarm: Make sure your intruder alarm is set and that the remote signalling is in place. Ensure sufficient numbers of keyholders are available to respond to an alarm activation within 20 minutes.

Maintenance: so far as is reasonably practical, there is an expectation that essential maintenance continues with any remedial measures completed. Premises that have Building Management Systems (BMS) with remote alerts should continue to be responded to. If possible, ensure gutters and drains are clear of debris, ahead of winter setting in.

Dangerous Goods: If you have any dangerous goods on your premises, ensure they are kept secure in their usual storage place, and review the inventory levels, documentation etc.

DISCLAIMER: This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.

KEY TAKEAWAYS:

Brokers are separate of all insurance companies, who act in your best interest and offer honest and non-partisan advice.

Use a broker for their industry/sector expertise, identifying day-to-day business risks, and for tailoring an insurance package that meets your needs.

Opting for a cheaper 'off the shelf' insurance policy is often not the best approach for insuring your business correctly - brokers can usually negotiate better premiums or conditions.

Small business owners tend to be born optimists – passionate, resilient and driven – but running a small business can certainly come with its own risks and challenges. That’s why it pays to have an insurance broker in your corner who can help accurately identify and protect the day-to-day risks your business faces.

Whatever business you're in, finding the right level of insurance should be top priority to ensure you are properly protected. However, insurance can be complicated to understand due to the broad range of risks businesses face, the various packages available and associated costs, and even the jargon in the contract and fine print that defines the terms & conditions.

'Using an insurance broker means clear advice, more choice and a better price tailored to your business needs'.

Price-conscious business owners usually believe if it is more cost effective going direct to the insurance provider. However this is often not the case, particularly with the multiple facets that are involved in operating a business these days.

'A broker ensures your claim is presented to the insurer in a clear and legible way to assist in a speedy settlement'.

A trusted adviser can add value to your business in a variety of ways that extend far beyond any initial cost saving you may find online. Some of these benefits include:

Market/sector expertise

Better rates

Accurate cover

Accurate valuations

Personal service

Unique offers

Access to specialists

Simplifying the fine print

Assistance with claims

In addition to the above benefits, specialised brokers (like Midland) also offer a range of value-added services such as assistance with claims, employee education and contract renewal support, all of which are included at no extra cost.

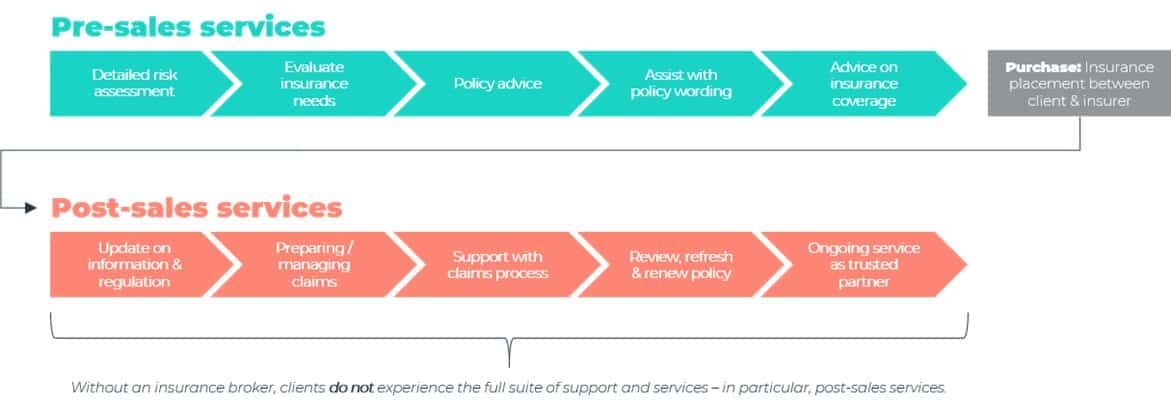

The below flow chart illustrates the typical journey that brokers take on with their clients, nurturing them through the entire insurance lifecycle from pre-sales service through to post-sales service. Without an insurance broker, clients don’t typically experience the full suite of support and services, in particular, the post-sales services.

'Remember, an insurance broker doesn't work for the insurance companies; they work for you and have a vested interest in the ongoing success of your business'.

Developing an ongoing business relationship with a broker can be of considerable benefit, but make sure you invest a little time and effort into finding one that's the right fit for you. Your broker should understand your future plans, the associated risks and how you like to do business. With those requirements ticked off, you can rest assured that they will continue sourcing the most suitable and most cost-effective cover that works for you and your business.

For further insights into the value that insurance brokers provide, Deloitte Australia released an in-depth research report in September 2020 that identified the benefits brokers bring to their clients, to insurers, to the economy, and to government and broader society. We summarised the report’s key findings, which you can view here.

Midland are a Steadfast Network Broker and a full-service brokerage.

With the number of confirmed cases of those infected with the coronavirus (COVID-19) growing every day, it has become somewhat of a nightmare for many countries and their economies.

The COVID-19 virus has already had a significant negative impact on the global economy, including the Australian economy. Recent import/export restrictions and sweeping travel bans have caused considerable disruption to both businesses and travellers alike. And understandably, one of the main concerns is around whether their insurance policies will respond should they be impacted by the outbreak.

As of the 23rd of January 2020, the Australian government placed coronavirus as a listed disease (i.e. a “known event”) under the Biosecurity Act 2015.

CORONAVIRUS & BUSINESS INTERRUPTION INSURANCE

For business package policies: once a disease becomes a “known event”, all, but a few, policies exclusions will take effect. This unfortunately means there is no insurance protection for disruptions to businesses arising from COVID-19.

Traditionally, business interruption policies only cover disruption to a business as a result of damage to ‘insured property’. However, over time, insurers widened the protection to provide coverage for things such as an outbreak of Legionnaires disease, or a measles outbreak which closes down one or two buildings disrupting a small number of businesses. A few policies have been known to provide coverage for an outbreak up to 50 kilometres from the business location, however most policies will only cover an infectious disease that occurs on the premises itself.

Ultimately, the cover afforded by both business packs and standard Industry special risks policies are not intended to cover disruption caused by an outbreak in a different state, let alone a different country.

CORONAVIRUS & TRAVEL INSURANCE

As of the 18th of March, the Australian Government issued a level 4 “do not travel” alert, applicable to all overseas destinations. This is their highest advice level.

For travel policies taken out before the 23rd of January 2020 – you may be covered for medical expenses that arise from contracting the disease overseas, and may even be covered for cancellation expenses. Make sure you also check with your broker or insurance provider as to whether your policy has specific exclusions around epidemics or pandemics.

For travel policies taken out on or after the 23rd of January 2020 – once a disease has been listed as an epidemic or pandemic, if you start a new policy you won’t be covered for any coronavirus-related claims. Insurers would expect that you entered the policy with the knowledge of potential loss.

For leisure travel policies (bought before 23/01/2020), you should be able to reclaim some of your lost expenses. Before you can do this, you'll need to see if your travel service provider is willing to refund you directly or provide some other alternative.

For corporate travel policies that were taken out or renewed before 23/01/2020 are likely to provide coverage for cancellation of trips to countries that are at ‘Level 4 - Do Not Travel’.

However, if you still decide to travel while the “do not travel” alert is in effect, your travel insurance policy will become void.

A number of major airlines have suspended or reduced flights all over the world, including Qantas, Virgin Australia and Jetstar. However, airlines are also offering refunds or free rescheduling services to affected customers, so you shouldn't be out of pocket for the cost of your ticket.

As for your other pre-paid travel expenses like accommodation, cruises or tours, you may be able to claim back your losses with travel insurance if your plans have been impacted by the cancellations or delays.

As with any other threat, it is also important to consider what risk management measures you can introduce to mitigate the risk to yourself, your business and the broader community. Below is a list of health and safety tips to help avoid infection and minimise the spread of coronavirus.

HEALTH & SAFETY TIPS

Wash your hands with soap when visibly dirty, after preparing food, using the bathroom, blowing your nose or sneezing, and after handling rubbish.

Apply alcohol-based hand sanitiser frequently throughout the day.

Avoid biting your nails, putting hands in your mouth or rubbing your eyes.

Boost your immune system by eating well, exercising, having enough sleep, and keeping your stress levels under control.

For organisations

Implement a work-from-home regime for employees

Cancel any non-essential business travel

Provide sanitised hand washing stations for use by staff and visitors.

Protect the mental wellbeing of employees concerned about the coronavirus.

For travellers

Follow the advice of local authorities as well as travel warnings stated by the WHO and Smartraveller websites.

Wash your hands often with soap and water or alcohol-based hand sanitiser, particularly after coming in contact with animals or animal products.

Remain alert for updates and advice from the relevant authorities on additional steps to manage the spread of the disease.

If you have any questions about your existing policy and would like to speak with one of our brokers, please give our Melbourne office a call on 03 9340 0100, or Sydney office on 02 9634 0900.

DISCLAIMER: This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.