COVID 2020 - a thank you to the transport industry.

From all of us at Midland Insurance Brokers, we wanted to say thank you to all workers within the transport industry for your commitment and support throughout the COVID-19 pandemic.

Through social distancing rules to keep infection rates down, panic buying of toilet paper & hand sanitiser, a sudden wave of trackpant sales, and the benching of all televised sport, the transport industry remained vigilant and committed to doing what it does best - keeping the country moving.

As the National Transport Industry's CEO, Tony Clark put it, "these are the people who work tirelessly every day to ensure Australians get what they need. We’ve seen an amazing response from these workers during the COVID-19 crisis and it’s now more than ever we can see how vital their work is."

As transport insurance specialists, we understand that each business has its own complexities and it is our role as insurance brokers to work with our clients to customise an insurance policy for each individual business. Then on your behalf, we will negotiate with numerous insurance companies to achieve a suitable premium and coverage for you, our client.

We specialise in providing tailored insurance for the transport industry, and strive to uncomplicate the complexities of the insurance world.

This year has been one of the toughest in living memory for the Australian alcohol industry, and with government restrictions around COVID-19 beginning to ease, many will be hoping to put the worst behind them.

Reopening a business in the post COVID-19 era presents a host of challenges, and we have tried to address the main ones below. However above all, it’s essential to keep abreast of current guidelines issued by federal and state governments via www.safeworkaustralia.gov.au and your local state government website respectively.

Engage with your customers: Check in on social media, leverage your existing customer base and get people excited about coming back to your cellar door, distillery or brewery. Anticipate how customers’ behaviour and expectations may have changed and try to accommodate their new expectations.

Think about how your processes will change: Think about how staff will work differently than before. Put in place a cleaning roster and make sure everyone is across the rules on social distancing. Consider common touch points; menus or tasting lists may be laminated and disinfected between uses, shared condiments, water stations removed etc. Set up training sessions to introduce staff to these new processes.

Consult with your staff: Many will have legitimate concerns about a return to work, from transport to at-risk loved ones, and shared facilities. It’s important to be open about your plans and address these concerns in order that staff can feel comfortable returning to work.

Check in on your assets and inventory: If you haven’t looked in on your stock or cellar door for a while, then it’s probably time to do so. Leaks may have sprung up, stock could have been damaged or use by dates exceeded, or machines may need essential maintenance. Consider stock levels in terms of reduced demand and make sure any replacement stock is ordered far enough in advance, as supply times may have increased.

Diversify: Many businesses have been forced to diversify their offerings, with increased delivery services, interactive online tasting experiences, and curated mixed cases giving customers the feeling of a cellar door experience at home. In some cases, these will continue as profitable side-lines, or even take over as a more significant part of the business.

Midland Insurance Brokers has functioned as a family-owned and operated business for more than 30 years, priding themselves on providing professional, personal and authentic insurance advice and service to Australian small and medium-sized enterprises (SMEs).

Terry Lane was awarded the coveted Lex McKeown trophy in 2014.

Midland commenced in 1986 as Cilmi Insurance Brokers, with aspirations for the company to be seen by their clients as an honest, reliable and professional insurance adviser with service excellence. And it turns out these values have served the company well, with strong client growth and retention, coupled with a strong reputation across the industry for good business ethics and a personal approach to their clients.

Over the last 5 years alone, Midland has doubled their number of staff, currently employing 50 staff across offices in Melbourne, Mornington Peninsula, Sydney and Perth, with plans in place to open offices in Queensland and South Australia to help better serve their growing client base.

In addition to providing a full range of general insurance products, Midland have also worked with various insurance companies to develop a suite of tailored insurance programs specifically for the industries below. Creating these programs has enabled Midland to negotiate additional benefits and exclusive discounts for their clients.

Interior Fitout

Breweries & Distilleries

Cideries & Kombucha Manufacturers

Wineries & Vineyards

Photography / Film & TV

Transport & Logistics

Landscapers & Horticulturalists

Trades & Construction

Throughout his successful tenure at Midland, Terry Lane accrued countless achievements, one of which was the coveted Lex McKeown trophy in 2014. Awarded by the National Insurance Brokers Association (NIBA), Terry was recognised for his outstanding service and contribution to the industry. Although, he could have probably won the award on account of his larger-than-life personality alone.

Terry was heavily involved in educating the industry and promoting how SMEs could benefit from using an insurance broker. For starters, insurance brokers:

are autonomous of insurers

provide honest and non-partisan advice

negotiate better premiums & conditions

explain all aspects of your policy

offer a wide range of plans

provide extensive market expertise

save you considerable time and effort

meet with you face to face

help with making a claim

help with employee education & contract renewal

work for you

He also had a knack for being able to communicate and simplify the complexities of insurance contracts to his clients. Uncomplicating the complex has been instilled in the company’s culture to this day and has subsequently become the company’s brand tagline.

Since Terry’s passing in 2018, his two sons, Damien and Justin, stepped up to take over the reins of the business, both of whom have been committed in maintaining the culture, values and business acumen that have been the backbone of Midland’s service offering to clients and insurers for the last 30 years.

As Justin sees it, “even though we’ve taken on more of a leadership and managerial role over the last couple of years, we still love being brokers and we will always make time to meet with our clients”.

For Damien, he finds “our terrific staff, our expertise and our simplified approach that we take with our clients is what makes Midland unique”.

For brother’s who work together, they not only complement each other’s skillset, they show that they have the drive and the ability to ensure the success of Midland’s future.

In order to help bring Midland further into the insurance industry spotlight, they have recently given their brand a refresh after 20 years. Damien states, “with the launch of an updated logo, colour suite and new website, we are determined to showcase Midland as a progressive and modern competitor in the insurance broker market”.

And although COVID-19 has played havoc on the operations of many SMEs around the country, Midland’s staff have been lucky enough to maintain ‘business as usual’ operations.

“Thankfully, it’s been a fairly seamless transition for us. We place great trust in our staff, and other than having to adapt to working from home and replacing face-to-face client meetings with Zoom or Skype, the Midland team has been able to continue serving clients remotely”, says Damien.

How the COVID-19 pandemic will impact the overall insurance industry moving forward is yet to be seen. But considering a brokers’ bread and butter revolves around risk management and adapting to change, Midland look to remain focused on doing what they do best – uncomplicating the complex world of insurance for their clients, tailoring policies to suit the individual needs of businesses….and holding on to the pipe dream that Carlton will win another premiership.

With many individuals having moved to remote working due to the coronavirus, it has unfortunately given opportunistic hackers and scammers greater opportunity to use the pandemic as a subject-matter for cyber attacks.

Malware (short for “malicious software”), is the general term covering all the different types of threats to your computer safety such as viruses, spyware, ransomware, phishing scams, worms, trojans, bots, and rootkits. It is basically a program designed to infiltrate a computer system, either by disrupting, damaging or simply gaining unauthorised access to your data.

The top 5 malware threats targeting small-to-medium businesses

1. Ransomware – once inside your device or network it denies access to systems or files until a ransom is paid.

2. Viruses – infect and corrupt software installed on devices, and then reproduce. A worm is a type of virus that once inside a vulnerable system can spread on its own.

3. Adware – software that displays unwanted advertisements on your computer, serving you pop-up ads, changing your browser’s homepage or adding spyware.

4. Phishing Emails – emails pretending to be from a legitimate business in order to trick you into giving out personal information (e.g. bank account numbers, passwords and credit card numbers).

5. Spyware / Keyloggers – records keystrokes and uses that information to steal passwords and other sensitive information, such as banking details.

'Almost one in three Australian adults were affected by cybercrime in 2019.'

How to prevent getting malware

The Australian Cyber Security Centre (ACSC) recommends implementing the below simple cyber security practices if you are working from home – during COVID or otherwise.

Minimise visits to unknown websites and avoid being enticed by clickbait.

Do not click on any links or open attachments from emails claiming to be from a trusted organisation (like your bank), or who are asking you to update or verify your details. Just press delete.

Use trusted sources of information – look for the padlock symbol and 'https' in the internet browser address bar.

Turn on multi-factor authentication across your devices as it can act as a safeguard when your password becomes compromised. Most sites & programs have the option to turn it on in their settings, especially the big players like iCloud, Microsoft 365, Outlook and Google/Gmail.

Install and regularly update anti-virus and anti-ransomware software.

Keep your operating system and software up to date with the latest versions

Secure your devices and use trusted Wi-Fi

Use a virtual private network (VPN). They add a layer of protection to your online activities and anyone who tries to spy on you.

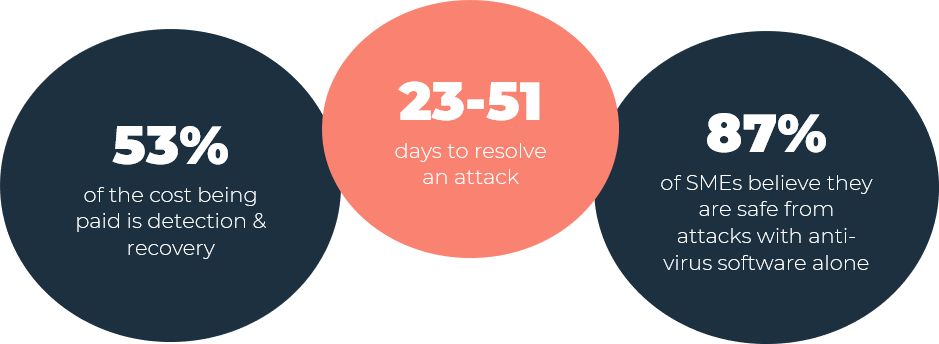

Ransomware is the number 1 form of malware threatening Australian businesses and is often unleashed when an unwitting employee clicks on an emailed link that contains malware. Once launched, the ransomware scrambles or deletes all data until a ransom is paid to restore it.

'Australia holds the highest rate of ransomware attacks against small-to-medium-sized enterprises (SMEs)'.

Since the COVID-19 lockdown

Since March 10th 2020, there has been a noticeable increase in COVID-19 themed ransomware attacks, with hackers likely gaining access through sophisticated phishing techniques targeted to employees working from home.

'94% of malware is delivered via email'.

Below are some of the most recent ransomware attacks that have impacted Aussie businesses since the COVID-19 lockdown.

1. Toll Group had some of their customer data stolen after suffering a major ransomware attack in January, followed by a second attack only a few months later.

2. Money management company MyBudget was attacked as it moved its employees to work-from-home arrangements amid coronavirus, causing a nationwide systems outage that left 13,000 customers in financial limbo.

3. BlueScope Steel was the subject of a ransomware attack in one of its US-based businesses, forcing production systems to be halted company-wide.

4. Service NSW was hacked in April, in an attack that compromised 47 staff email accounts.

Whether or not the ransom ends up being paid to the hackers, the indirect costs to a business from simply spending the time to detect and resolve a malware attack can be incredibly costly – on average, businesses suffer a 28% information loss, 25% revenue loss and 29% productivity loss.

'The average cost of downtime as a result of a ransomware attack is $208,000 – a 200% increase on 2018'.

With many businesses offering a 'hybrid' working model these days, it's now more important than ever to remain vigilant against the threat of cyber attacks.

Put as many of the above prevention techniques as you can in place, with emphasis on implementing multi-factor authentication and a password manager to help safeguard you against any future destructive computer viruses.

To further provide you and your family with added peace of mind and the confidence in knowing that you’re covered should you fall victim to a cyber-attack, Midland now offer a stand-alone personal cyber insurance policy. Cover starts from as little as $99 per year.

In the meantime, if you think you might have provided your account details to a scammer, contact your bank or financial institution immediately. The Australian government also encourages you to report scams to the ACCC via their report a scam page.

DISCLAIMER: This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.

KEY TAKEAWAYS

Parametric insurance is based on a ‘triggered’ event rather than a claim for actual harm or loss. It’s an insurance alternative that’s good for the customer and it looks like it’s here to stay. It basically covers the probability of a predefined event happening and pays out an agreed amount instead of compensating for the actual loss incurred. Claims are settled quickly, the payout is certain, and it allows the customer to plan ahead.

Although still in its infancy in Australia, it is likely to show strong growth over the coming years as triggers can be better defined, especially as AI and robotics allow technology to make decisions, replicate human actions at scale and with precision.

The future of parametric cover could see it applied across a wide range of industries and events, including agriculture, tourism & travel, retail, shipping, natural landmarks impacted by climate change, terrorism and even brand sentiment.

What is Parametric Insurance?

Parametric insurance is growing at a rapid pace around the world and is being praised as an attractive alternative to some traditional insurance policies.

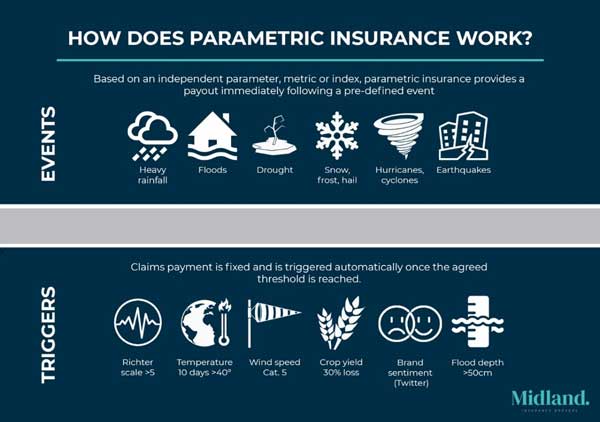

Even if it does sound a little complex, parametric insurance (or event-based insurance) is simpler than traditional cover. Compared to a typical insurance claim which compensates for harm or loss, parametric insurance pays out a pre-agreed amount based on a ‘triggered’ event using objective data sets that neither the insurer nor client controls.

“Global parametric premiums have reached $US5 billion and are growing by 6-9% every year”.

When could parametric insurance be used?

Natural catastrophes or extreme weather events are currently the most prominent triggers as they can be defined by magnitude (e.g. earthquakes, tropical cyclones, floods), or wind speed or precipitation metrics. However, there are also other applications where payouts can be calculated using robust data points, including triggers for market indices, power outages, crop yields or even online sentiment for insuring a brand’s value.

How does parametric insurance work?

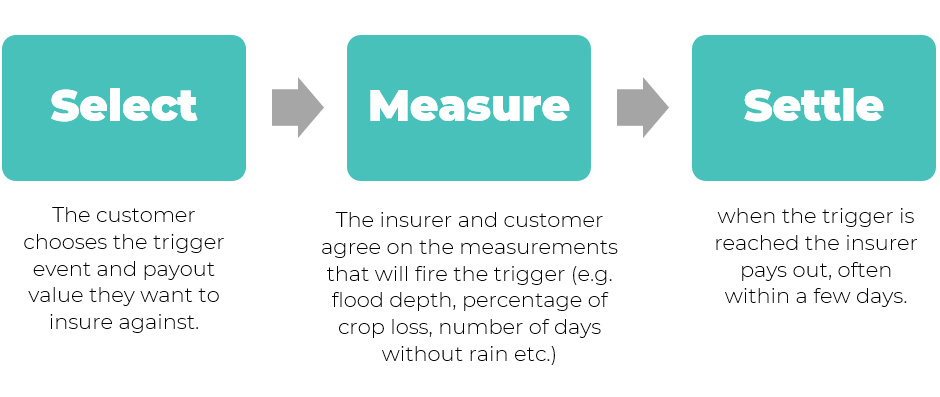

Below are a few case studies of how parametric insurance has been implemented throughout the world, followed by a couple of opportunities closer to home that we could potentially see put in place.

Case Studies

Case study 1: global insurance company, CelsiusPro, worked with the Ethiopian government to cover 15 regions and 6,500 farmers across the country with parametric insurance, so that in the event of a drought the farmers get paid out by the government. (Source: ABC News)

Case study 2: an owner of an open-pit salt mine in northern Australia was required to evacuate the site in the probable event of a cyclone. As a result, the owner had to undertake costly and time-consuming geotechnical studies before operations could resume. To address the problem, a parametric product was offered which would pay out in the event of a tropical strength cyclone. The payout would be triggered if the cyclone fell within 100 kilometres of the mine. (Source: qic.com.au)

Case study 3: In January 2019, Swiss Reinsurance Co. launched FLOW, a parametric water-level insurance product designed to protect companies from the financial impact of high or low river water levels. The direct physical effects of low water levels are almost non-existent, but the indirect costs to businesses that depend on rivers can be significant. (Source: Corporate Solutions Swiss)

Opportunities

Opportunity 1: after the expensive drought bail-outs of 2014 and 2018 in Australia, and the effects of climate change likely to bring more droughts in the years to come, parametric insurance within the agricultural industry is being taken a lot more seriously. With the addition of hundreds of new meteorological stations over the past decade and the rapid advancement in technology, farmers and insurers can now more accurately evaluate trigger data and forecast how acute their risk is of an intense dry period, wet harvest or even the potential for frost. This makes it particularly helpful for farmers in remote areas like much of the WA and NSW wheat belts.

For example, cover could be agreed at $1M based on there being more than 30 days of frost during winter (like many parts of NSW saw in 2018), and should that target be exceeded, the farmer would be paid out the $1M regardless of the damage suffered or the costs incurred to replant the crop. Cover could also even be implemented as little as 15 days out before harvest.

With extreme weather events causing up to 70% of crop loss in Australia, parametric insurance can give farmers added protection and greater confidence for their farming future.

Opportunity 2: a 2019 report by global firm Clyde & Co recommended implementing a risk management plan for the Great Barrier Reef in order to guarantee its long-term resilience against climate change and potential catastrophic events. Where there was previously no option for cover of the reef, parametric insurance can provide the $56B tourism asset with a security blanket, protecting it against any further coral bleaching, ocean acidification or pollution.

What are the benefits of parametric insurance?

Parametric insurance opens up a new avenue for risk coverage and can provide significant benefits to both insurer and customer.

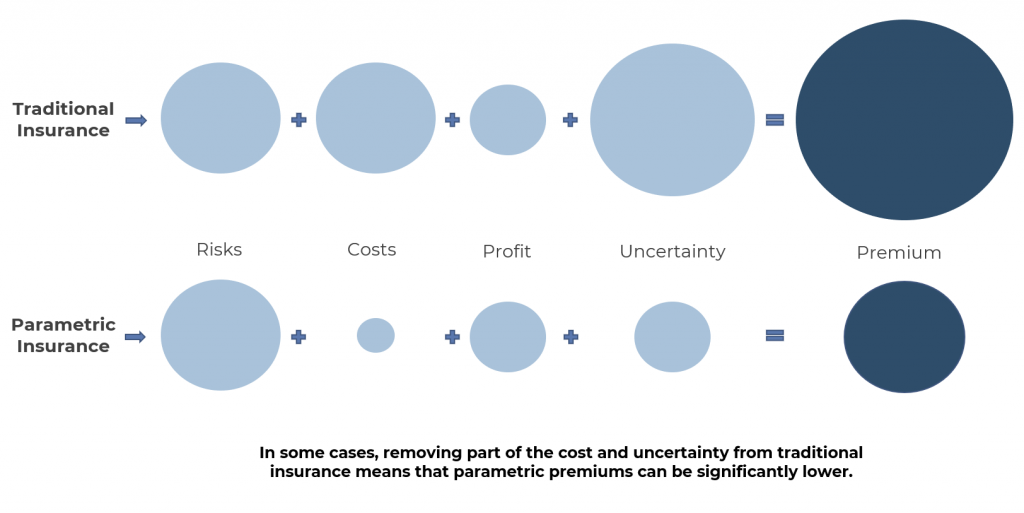

People in areas hit by a catastrophic event in the past would find it very difficult to get cover on a traditional policy as the risk involved is simply too high. By insuring against the likelihood of an event happening as opposed to actual damage caused, parametric insurance reduces the cost and uncertainty for those who have previously been excluded.

It is able to service remote customers

As parametric insurance relies on data to pay and assess claims, it becomes a lot easier for insurers to be able to assess and pay claims for those that live in remote areas. For example, a farmer’s crop can be covered based on agricultural indices such as crop yield, excessive temperatures or heavy rainfall.

It provides a transparent claims process

Parametric insurance relies on a pre-agreed payout, so claims are processed quickly and efficiently. There is minimal paperwork required, no lengthy claims investigations and no disputes. With such a seamless process in place, it can also end up improving the overall customer and brand experience.

It’s becoming a valuable asset for brokers

Parametric insurance adds another valuable tool to a broker’s tool box. It gives them the opportunity to fill the gaps left by a traditional insurance policy, or the option to provide a policy that couldn’t be placed previously. Brokers can ultimately provide clients with a policy that is all-encompassing, alleviating any uncertainty.

The future of parametric insurance

Although the market for parametric solutions in Australia is still in its infancy, its possibilities are only just being realised.

Advances in data science, sensor technology and artificial intelligence have enabled vastly superior data collection and analysis methods to be developed. Over time, this will allow insurers to evolve the modelling of data and indexes upon which payout triggers are based, price cover more accurately and provide a more bespoke selection of cover across a variety of industries.

With artificial intelligence at the forefront, the new generation of parametric insurance solutions could include protection for things like cities and airports in the event of terrorism, coverage for shipping and manufacturing companies when river water-levels fall, solutions for retailers in the event of reduced foot traffic during strikes, or economic assistance for hotels in the event of infectious disease outbreaks.

Just as many products and services have evolved by taking advantage of improvements in data science, parametric insurance cover looks to provide a more efficient insurance product that’s fitting for the modern age.

DISCLAIMER: This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.

Key takeaways:

Management Liability (ML) Insurance covers directors and officers against the exposures & risks that come with managing a business.

An ML policy protects you and your business against things like: OH&S dramas, harassment, defamation, fines, fraud, theft and data breaches.

ML claims have increase 300% over the last 5 years, with the average penalty awarded against companies costing $62,000.

There are a multitude of risks facing small businesses in Australia’s challenging economic environment today. New and often complex legislation are always on the horizon where companies can also expect increased exposure to liability and fraud.

"As a business owner, you automatically take on the risk of being personally liable for the consequences of any unintended errors arising from your own daily actions, or even the actions of your employees".

The changing regulatory environment in Australia has increased the operating risks for businesses of all sizes – workplace accidents are now subject to high statutory scrutiny; employee theft is on the rise, while employment and commercial disputes are becoming more and more expensive to resolve.

If you’re a business owner, director or senior manager/officer of a private company, you automatically take on the risk of being personally liable for the consequences of unintended errors arising from your own daily actions, or even the actions of your employees.

WHY SHOULD YOU INVEST IN MANAGEMENT LIABILITY INSURANCE?

Irrespective of industry or company size, without adequate protection you could risk losing not only your business, but also your personal assets – such as your home – from being sold to cover the cost of paying claims. This insurance protects you personally, and therefore your wealth and lifestyle.

Claims can also be brought against directors and officers from every angle. Disgruntled shareholders, customers, investors, employees, competitors, regulators and creditors all have a legal entitlement to launch action if they feel directors and officers have not lived up to their responsibilities.

WHAT CAN A MANAGEMENT LIABILITY POLICY COVER YOU FOR?

The three most common management liability claims are for employment practices such as bullying, harassment and wrongful dismissal. But ML covers a range of risk exposures affecting directors and officers of private companies.

"Claims can be brought against senior management from every angle, including disgruntled shareholders, employees, customers or competitors".

Many businesses think it won’t happen to them, but statistics show otherwise.

MANAGEMENT LIABILITY INSURANCE CLAIMS EXMPLES:

A customer database was illegally breached, and personal information was compromised. The costs of advising the customers plus the legal representation were covered by their ML policy.

A manufacturing employee manipulated the accounts payable system to create non-existent customers and generated purchase orders and invoices to transfer money to the fake accounts, by accessing other employee authorisation details. An internal audit eventually discovered the total losses.

A senior employee is dismissed after lodging complaints of bullying and aggressive conduct by the managing director. Complaints are also made of racial discrimination and disability discrimination. Action is commenced in the Federal Court and the matter is settled for a 6-figure sum.

WHO CAN BRING AN ML CLAIM AGAINST A COMPANY, ITS DIRECTORS, OFFICERS AND EMPLOYEES?

Regulators (e.g. ACCC, ASIC, the ATO)

Employees

Competitors

Creditors

Shareholders

Clients

Liquidators/Administrators

WHAT USUALLY ISN'T COVERED IN THE POLICY?

Generally, the policy won’t cover cyber-crime (unless specifically set out in your policy), employee entitlements, property damage or bodily injury. There may be other exclusions included in your policy which your broker can outline for you.

Without Management Liability insurance, you become exposed to significant financial loss, disqualification from your position, or even bankruptcy. With such penalties, it shows there is a clear need for an effective way to protect your business.

So why take even the slightest chance of putting your business or personal assets at risk? ML cover can provide you with peace of mind, leaving you to focus on what you do best.

DISCLAIMER: This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.

Continuity of business is a significant issue for employers and their employees during this unprecedented and difficult time. FairWork Australia have developed the below coronavirus information to help employees and employers understand how coronavirus impacts Australian workplace laws.

Find out about your workplace entitlements and obligations if you're affected by the outbreak of covid-19, including information about stand-downs from work, working arrangements impacted by school closures, and pay and sick leave entitlements.

Arranging Flexible Work

There are a range of flexible working arrangements that employers and employees can explore together. These include:

working from home

changing the number of hours an employee works

changing the start or finish times of employees' shifts

changing patterns of work, such as rostering arrangements

changing the type of work done by employees.

Employers and employees need to consider and comply with any requirements under the Fair Work Act, an applicable award, enterprise agreement, employment contract or workplace policy.

Using paid leave

Employers and employees are encouraged to explore options that enable an employee to take their accrued leave entitlements during the coronavirus outbreak. Options include:

taking accrued annual leave

taking any other paid leave (such as long service leave or paid leave available under an award, enterprise agreement or employment contract)

directing employees to take accrued annual leave in certain circumstances

taking any other paid leave by agreement between the employee and the employer.

Using unpaid leave

In many circumstances, employees won’t have access to paid leave during the coronavirus outbreak. For example, if they are permanent but have already used all their accrued leave entitlements. In these situations, employers and employees can agree for an employee to take unpaid leave.

Under the Fair Work Act, unpaid leave is also available for employees in certain circumstances, such as unpaid carer’s leave for casual employees.

Standing down employees

Employers may be able to stand their employees down without pay during the coronavirus outbreak for a number of different reasons. These can include where:

the business has closed because of an enforceable government direction relating to non-essential services (which means there is no work at all for employees to do even from another location)

a large proportion of the workforce is in self-quarantine meaning the remaining employees can’t be usefully employed

there’s a stoppage of work due to lack of supply for which the employer can’t be held responsible.

Importantly, employees can be stood down without pay under the Fair Work Act if they can’t be usefully employed because of a stoppage of work for any cause for which the employer can’t reasonably be held responsible.

If other options have been exhausted, or if they aren’t feasible, some employers may need to make their employees’ positions redundant in response to a business downturn caused by the coronavirus outbreak. Where this happens, employers must make sure they comply with any requirement to notify and consult about the redundancies under an applicable award, enterprise agreement, employment contract or workplace policy, and make reasonable efforts to find their employees other jobs.

They also need to provide those employees with their correct entitlements, which may include notice, redundancy pay and payment of any accrued leave entitlements.

The Fair Work Act protects employees from being dismissed for a number of reasons, including:

because they are temporarily away from work because they are sick (such as with coronavirus)

discrimination

any reason that is harsh, unjust or unreasonable or another protected right.

During these challenging and unprecedented times, some businesses may need to close because they are no longer profitable or run out of money.

This can mean that employees lose their jobs, and in some cases where a business is bankrupt or goes into insolvency, employers may not be able to pay their employees the wages and entitlements they’re owed.

When an employer is bankrupt, or goes into liquidation or insolvency, employees may be able to get help through the Fair Entitlements Guarantee (link below).

Sometimes, an employer might close their business and abandon it without placing it into liquidation. Where this happens, the Australian Securities and Investments Commission (ASIC) may be able to help recover unpaid employment entitlements.

Please refer to coronavirus.fairwork.gov.au for further information relating to the above. This page also houses links to advice on health, childcare, business support, workplace health & safety, tax & superannuation and online safety.

Finally, visit www.australia.gov.au for the latest coronavirus news, updates and advice from government agencies across Australia.

DISCLAIMER: This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.

Temporary Closure Due to the coronavirus restrictions, many businesses are having to temporarily close and allow staff to help sustain operations via home working. We wanted to give you some general advice about how to protect your premises during any temporary closures. This guidance is from a risk management perspective. Please give us a call should you have any queries relating to insurance cover.

Risk Control Measures:

Waste: Remove all external waste, pallets and empty skips ahead of closing.

Waste bins: Empty all waste bins and relocate to a secure area, ideally at least 10 metres from the building. If this is not possible and bins and skips are within 10m, these should have lockable lids.

Fire Systems: Ensure that any fire and/or sprinkler systems are fully operational

Fire Doors: Carry out a check to ensure that internal fire doors are closed

Building Utilities: Shutdown any non-essential electrical devices and building utilities. Isolate nonessential services, gas valves etc.

Inspections: Where at all possible (and subject to Government restrictions) try to implement periodic inspections of the building (internally and externally). Please ensure that you comply with existing government guidance regarding vulnerable people and lone worker risk assessments. Consider the provisioning for alternative skilled personnel, such as security guarding/patrolling companies.

Physical Security: Carry out a check to ensure physical security measures are in place e.g. fences are in good repair, windows are locked, shutters are in place, gates are locked.

Intruder Alarm: Make sure your intruder alarm is set and that the remote signalling is in place. Ensure sufficient numbers of keyholders are available to respond to an alarm activation within 20 minutes.

Maintenance: so far as is reasonably practical, there is an expectation that essential maintenance continues with any remedial measures completed. Premises that have Building Management Systems (BMS) with remote alerts should continue to be responded to. If possible, ensure gutters and drains are clear of debris, ahead of winter setting in.

Dangerous Goods: If you have any dangerous goods on your premises, ensure they are kept secure in their usual storage place, and review the inventory levels, documentation etc.

DISCLAIMER: This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.

KEY TAKEAWAYS:

Brokers are separate of all insurance companies, who act in your best interest and offer honest and non-partisan advice.

Use a broker for their industry/sector expertise, identifying day-to-day business risks, and for tailoring an insurance package that meets your needs.

Opting for a cheaper 'off the shelf' insurance policy is often not the best approach for insuring your business correctly - brokers can usually negotiate better premiums or conditions.

Small business owners tend to be born optimists – passionate, resilient and driven – but running a small business can certainly come with its own risks and challenges. That’s why it pays to have an insurance broker in your corner who can help accurately identify and protect the day-to-day risks your business faces.

Whatever business you're in, finding the right level of insurance should be top priority to ensure you are properly protected. However, insurance can be complicated to understand due to the broad range of risks businesses face, the various packages available and associated costs, and even the jargon in the contract and fine print that defines the terms & conditions.

'Using an insurance broker means clear advice, more choice and a better price tailored to your business needs'.

Price-conscious business owners usually believe if it is more cost effective going direct to the insurance provider. However this is often not the case, particularly with the multiple facets that are involved in operating a business these days.

'A broker ensures your claim is presented to the insurer in a clear and legible way to assist in a speedy settlement'.

A trusted adviser can add value to your business in a variety of ways that extend far beyond any initial cost saving you may find online. Some of these benefits include:

Market/sector expertise

Better rates

Accurate cover

Accurate valuations

Personal service

Unique offers

Access to specialists

Simplifying the fine print

Assistance with claims

In addition to the above benefits, specialised brokers (like Midland) also offer a range of value-added services such as assistance with claims, employee education and contract renewal support, all of which are included at no extra cost.

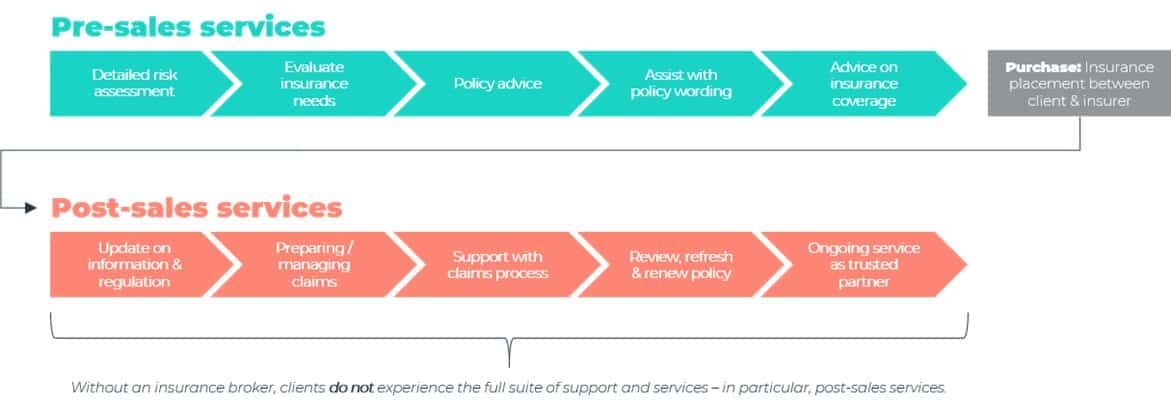

The below flow chart illustrates the typical journey that brokers take on with their clients, nurturing them through the entire insurance lifecycle from pre-sales service through to post-sales service. Without an insurance broker, clients don’t typically experience the full suite of support and services, in particular, the post-sales services.

'Remember, an insurance broker doesn't work for the insurance companies; they work for you and have a vested interest in the ongoing success of your business'.

Developing an ongoing business relationship with a broker can be of considerable benefit, but make sure you invest a little time and effort into finding one that's the right fit for you. Your broker should understand your future plans, the associated risks and how you like to do business. With those requirements ticked off, you can rest assured that they will continue sourcing the most suitable and most cost-effective cover that works for you and your business.

For further insights into the value that insurance brokers provide, Deloitte Australia released an in-depth research report in September 2020 that identified the benefits brokers bring to their clients, to insurers, to the economy, and to government and broader society. We summarised the report’s key findings, which you can view here.

Midland are a Steadfast Network Broker and a full-service brokerage.

With the number of confirmed cases of those infected with the coronavirus (COVID-19) growing every day, it has become somewhat of a nightmare for many countries and their economies.

The COVID-19 virus has already had a significant negative impact on the global economy, including the Australian economy. Recent import/export restrictions and sweeping travel bans have caused considerable disruption to both businesses and travellers alike. And understandably, one of the main concerns is around whether their insurance policies will respond should they be impacted by the outbreak.

As of the 23rd of January 2020, the Australian government placed coronavirus as a listed disease (i.e. a “known event”) under the Biosecurity Act 2015.

CORONAVIRUS & BUSINESS INTERRUPTION INSURANCE

For business package policies: once a disease becomes a “known event”, all, but a few, policies exclusions will take effect. This unfortunately means there is no insurance protection for disruptions to businesses arising from COVID-19.

Traditionally, business interruption policies only cover disruption to a business as a result of damage to ‘insured property’. However, over time, insurers widened the protection to provide coverage for things such as an outbreak of Legionnaires disease, or a measles outbreak which closes down one or two buildings disrupting a small number of businesses. A few policies have been known to provide coverage for an outbreak up to 50 kilometres from the business location, however most policies will only cover an infectious disease that occurs on the premises itself.

Ultimately, the cover afforded by both business packs and standard Industry special risks policies are not intended to cover disruption caused by an outbreak in a different state, let alone a different country.

CORONAVIRUS & TRAVEL INSURANCE

As of the 18th of March, the Australian Government issued a level 4 “do not travel” alert, applicable to all overseas destinations. This is their highest advice level.

For travel policies taken out before the 23rd of January 2020 – you may be covered for medical expenses that arise from contracting the disease overseas, and may even be covered for cancellation expenses. Make sure you also check with your broker or insurance provider as to whether your policy has specific exclusions around epidemics or pandemics.

For travel policies taken out on or after the 23rd of January 2020 – once a disease has been listed as an epidemic or pandemic, if you start a new policy you won’t be covered for any coronavirus-related claims. Insurers would expect that you entered the policy with the knowledge of potential loss.

For leisure travel policies (bought before 23/01/2020), you should be able to reclaim some of your lost expenses. Before you can do this, you'll need to see if your travel service provider is willing to refund you directly or provide some other alternative.

For corporate travel policies that were taken out or renewed before 23/01/2020 are likely to provide coverage for cancellation of trips to countries that are at ‘Level 4 - Do Not Travel’.

However, if you still decide to travel while the “do not travel” alert is in effect, your travel insurance policy will become void.

A number of major airlines have suspended or reduced flights all over the world, including Qantas, Virgin Australia and Jetstar. However, airlines are also offering refunds or free rescheduling services to affected customers, so you shouldn't be out of pocket for the cost of your ticket.

As for your other pre-paid travel expenses like accommodation, cruises or tours, you may be able to claim back your losses with travel insurance if your plans have been impacted by the cancellations or delays.

As with any other threat, it is also important to consider what risk management measures you can introduce to mitigate the risk to yourself, your business and the broader community. Below is a list of health and safety tips to help avoid infection and minimise the spread of coronavirus.

HEALTH & SAFETY TIPS

Wash your hands with soap when visibly dirty, after preparing food, using the bathroom, blowing your nose or sneezing, and after handling rubbish.

Apply alcohol-based hand sanitiser frequently throughout the day.

Avoid biting your nails, putting hands in your mouth or rubbing your eyes.

Boost your immune system by eating well, exercising, having enough sleep, and keeping your stress levels under control.

For organisations

Implement a work-from-home regime for employees

Cancel any non-essential business travel

Provide sanitised hand washing stations for use by staff and visitors.

Protect the mental wellbeing of employees concerned about the coronavirus.

For travellers

Follow the advice of local authorities as well as travel warnings stated by the WHO and Smartraveller websites.

Wash your hands often with soap and water or alcohol-based hand sanitiser, particularly after coming in contact with animals or animal products.

Remain alert for updates and advice from the relevant authorities on additional steps to manage the spread of the disease.

If you have any questions about your existing policy and would like to speak with one of our brokers, please give our Melbourne office a call on 03 9340 0100, or Sydney office on 02 9634 0900.

DISCLAIMER: This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.