This will relate to claims where there have been damages caused to your property (buildings, contents or stock) from a one-off event such as water (burst pipe), storm (rainwater, wind, hail etc), fire, burglary, impact or some other form of accidental damage.

What you can do - 'Make Safe Works' (temporary repairs)

Immediately after an event, under the terms of all insurance policies, there is a ‘Make Safe Works’ provision which allows you to undertake temporary works to ensure peoples’ safety and prevent further damages. You don’t need your insurer’s consent when undertaking these works. As long as the costs are reasonable and the claim is accepted, these costs will be covered under the claim.

What you must not do

All policies state that you must not undertake any permanent works/repairs without the insurer’s consent. This does not apply to the Make Safe Works as explained above.

There is a notable exception to this; If you are attempting to mitigate the loss of income to your business as the result of an event, an argument can be made for you undertaking works promptly if able to do so. As long as the costs are reasonable, and you can show it prevented or minimised the business income loss, the insurer should accept this.

Causation – Reports (what caused the damage)

If you are undertaking any work, it is important that the attending trade provides a detailed report on how the damages have occurred. This should include photos. The cost of these reports are covered if the claim is accepted. The insurer needs this to determine if the damages are coverable under your policy or not. Without this, they will be unable to assess the claim and therefore may not cover the claim.

Quotes & Invoices

If you are undertaking work or getting suppliers to quote, it is important they are providing enough information for the insurer to assess if the costs of the work are fair and reasonable. Without this, they may not be able to assess your claim and they may withhold cover.

Each quote or invoice should include:

areas affected, including measurements – if multiple rooms are affected, each room needs to be listed separately with separate measurements for each.

material costs – each material item should be costed individually for each separate area (room) affected.

labour costs – how many people, the time required to complete the work and the hourly rate.

What is needed for a claim to be lodged

For each and every claim we will require:

the date the damages occurred or were first discovered

how the damages occurred e.g., water, fire, impact, accidental damage etc

what has been damaged

photos

invoices for any temporary Make Safe Works undertaken

quotes for remaining repairs

If you are unable to get anyone to undertake the temporary repairs/quote, or don’t have any trades you have a relationship with, all insurers do have panel builders who can undertake Make Safe Works and provide quotes for the insurable repairs.

As a business owner, safeguarding your enterprise from unforeseen circumstances is imperative to maintain its growth and longevity. Mitigating the financial impact of accidents, natural disasters, and legal disputes requires a safety net that can help your business recover and continue operating without disruption.

From general liability insurance to workers' compensation insurance and cyber liability insurance, there are many different types of business insurance available to protect your business. Each type of insurance provides coverage for different risks, making it important to understand your specific needs and choose the coverage that best meets them.

The Cost of Business Insurance: A Necessary Investment

While the cost of business insurance may seem high, the cost of not having insurance can be far greater. Without insurance coverage, your business is vulnerable to unexpected losses that can quickly drain your financial resources. By investing in the right insurance coverage, you can provide peace of mind to yourself and your employees and protect your business against unforeseen circumstances.

As a business owner in Australia, it's important to consider the cost vs. benefit of business insurance. According to the Insurance Council of Australia, small businesses in Australia are particularly vulnerable to natural disasters, with around 1 in 2 small businesses impacted by natural disasters. This highlights the importance of having property insurance in place to protect your business against unexpected losses.

In addition, according to the Insurance Council only 20% of SMEs have cyber insurance in place, despite 43% experiencing a cyber attack or breach. This highlights the need for small businesses to consider cyber liability insurance to protect against the increasing threat of cyber attacks.

Choosing the Right Insurance Coverage for Your Business

When choosing insurance coverage for your business, it's essential to carefully consider your options and select the coverage that best meets your needs. This may involve working with an experienced insurance broker who can help you identify the specific risks associated with your business and recommend appropriate coverage options. Additionally, it's important to consider the deductible and policy limits, ensuring that they're reasonable and justifiable based on the risks associated with your business.

Effective Risk Management Strategies

In addition to insurance coverage, implementing effective risk management strategies can help reduce the likelihood of accidents and injuries, and minimize the potential costs associated with liability claims and lawsuits. This may involve:

Conducting regular safety inspections.

Training employees on best practices, and:

Maintaining accurate records.

Legal and Regulatory Compliance for Business Insurance

It's also imperative that your business is in compliance with all relevant legal and regulatory requirements for insurance coverage. This may include obtaining specific types of insurance coverage required by state or federal law, as well as ensuring that your insurance coverage meets minimum standards for coverage limits and deductibles.

In conclusion, the importance of business insurance cannot be overstated. Protecting your business against the unexpected is essential for its continued success. By investing in the right insurance coverage, working with experienced insurance agents, and implementing effective risk management strategies, you can protect your business and ensure its continued growth and success. Don't wait until it's too late – invest in the security of your business today.

Small business owners in Australia face a challenging and ever-changing landscape, from economic uncertainty and fierce competition to regulatory compliance and cybersecurity threats. While these pressures can seem overwhelming, there are proven solutions to mitigate the risks.

In this article, we explore the top five concerns for small business owners in Australia.

Economic uncertainty: Staying afloat in turbulent times

Economic uncertainty can be a significant concern for Australian business owners, particularly in times of market volatility or global economic instability. Uncertainty around government policy changes, interest rates, and consumer spending can impact businesses of all sizes, making it difficult to plan for the future and make informed business decisions.

In a survey conducted by the Small Business Association of Australia, economic uncertainty is the primary worry for small business owners in the country. The survey found that 65% of respondents were worried about economic conditions, with 29% citing the risk of a recession or economic downturn as their biggest concern.

To navigate economic uncertainty, businesses may need to adopt a flexible and agile approach to their operations. This could involve diversifying their product or service offerings, exploring new markets, or investing in technology and innovation to stay ahead of the curve.

Fierce competition: Staying ahead of the game

Maintaining a healthy cash flow is essential for any business, but it can be particularly challenging for small and medium-sized enterprises (SMEs). Cash flow issues can arise due to a variety of factors, such as fluctuations in revenue, late payments from customers, or unexpected expenses.

The Australian Securities and Investments Commission (ASIC) states that cash flow is a key concern for small business owners. Cash flow issues can be particularly acute for SMEs, which may have limited access to financing or credit facilities.

To manage cash flow, businesses may need to adopt a range of strategies, such as implementing more rigorous invoicing processes, negotiating payment terms with suppliers, or seeking out alternative funding sources such as government grants or loans.

Competition is a fact of life for businesses in Australia, and staying competitive is crucial for maintaining long-term success. Competition can come from a variety of sources, including domestic and international players, new entrants to the market, or changes in consumer preferences.

Small businesses in Australia face tough competition, as noted by the Australian Trade and Investment Commission. To stay competitive, businesses may need to invest in research and development, marketing and branding, or operational efficiencies. Building strong relationships with customers and suppliers can also be crucial for maintaining a competitive edge.

Regulatory compliance: Operating within the law

Compliance with government regulations can be complex and time-consuming, and non-compliance can lead to penalties, fines, or legal action. Australian businesses are subject to a wide range of regulations at the federal, state, and local levels, covering areas such as taxation, employment law, and health and safety.

Small business owners in Australia may find government regulations to be a source of stress, particularly if they are new to the industry, according to Australian Government Business, with respondents identifying regulation as a significant concern. To manage regulatory compliance, businesses may need to invest in specialised expertise or seek out external advice from legal or accounting professionals. Implementing robust compliance processes and staying up to date with changes in regulations can also be essential.

Cybersecurity threats: Protecting against data breaches

In Australia, a majority of businesses (62%) have reported experiencing a cyber security incident, indicating the prevalence and severity of this issue. Such incidents, which include cyber attacks, data breaches, and other forms of cyber threats, can result in severe financial losses, reputational harm, and legal and regulatory liabilities. To manage cybersecurity risks, businesses may need to invest in specialised expertise, implement robust IT security protocols, and stay up to date with emerging threats and best practices.

Conclusion

Small business owners in Australia face many challenges that can threaten their businesses' stability and success. Economic uncertainty, cash flow, competition, regulation, and cybersecurity are significant concerns. However, investing in business insurance can provide a proven solution to several pressures. Business insurance protects Australian businesses from unexpected events and provides access to resources like risk management advice and legal assistance. It can also give small business owners a competitive edge by demonstrating responsibility and trustworthiness. Ultimately, business insurance is a valuable investment for small business owners looking to protect their businesses and position themselves for long-term success.

Broadly speaking, liability claims are where a third party has alleged some action or inaction which has caused a detrimental outcome, either legally or financially.

What can this look like?

Government agencies could pursue you for breach of regulation or legislation.

A person may have injured themselves on your property and are seeking compensation for things like medical costs and time off work.

It could be that someone has relied on some advice you have provided, and a negative outcome (actual or alleged) has occurred as a result.

What are you likely to receive that lets you know you may have a liability claim?

A writ from the courts – more often than not this will be a Statement of Claim.

Tribunal Documents – these will be similar to those from the courts.

Letter of Demand – this is a fairly standard letter which will outline what they say has caused their negative outcome and what they expect as a remedy.

Anything in writing – a text or email which alleges wrongdoing can also be considered.

What do you need to do?

As soon you receive anything, you should contact us so we can provide further advice as you may have a policy that will provide cover.

What are the implications for not advising us as soon as possible?

If a matter progresses significantly before we notify your insurer, they will state their position has been prejudiced. This could mean they may try to avoid covering the claim or they may only provide cover for a certain amount of costs you have incurred to date, and this could leave you substantially out of pocket.

Also, insurers often have specialist law firms familiar with legislation/regulation, particularly around insurance claims. This means they are often more able to attend to addressing the claim more effectively, usually meaning a better defense at reduced costs.

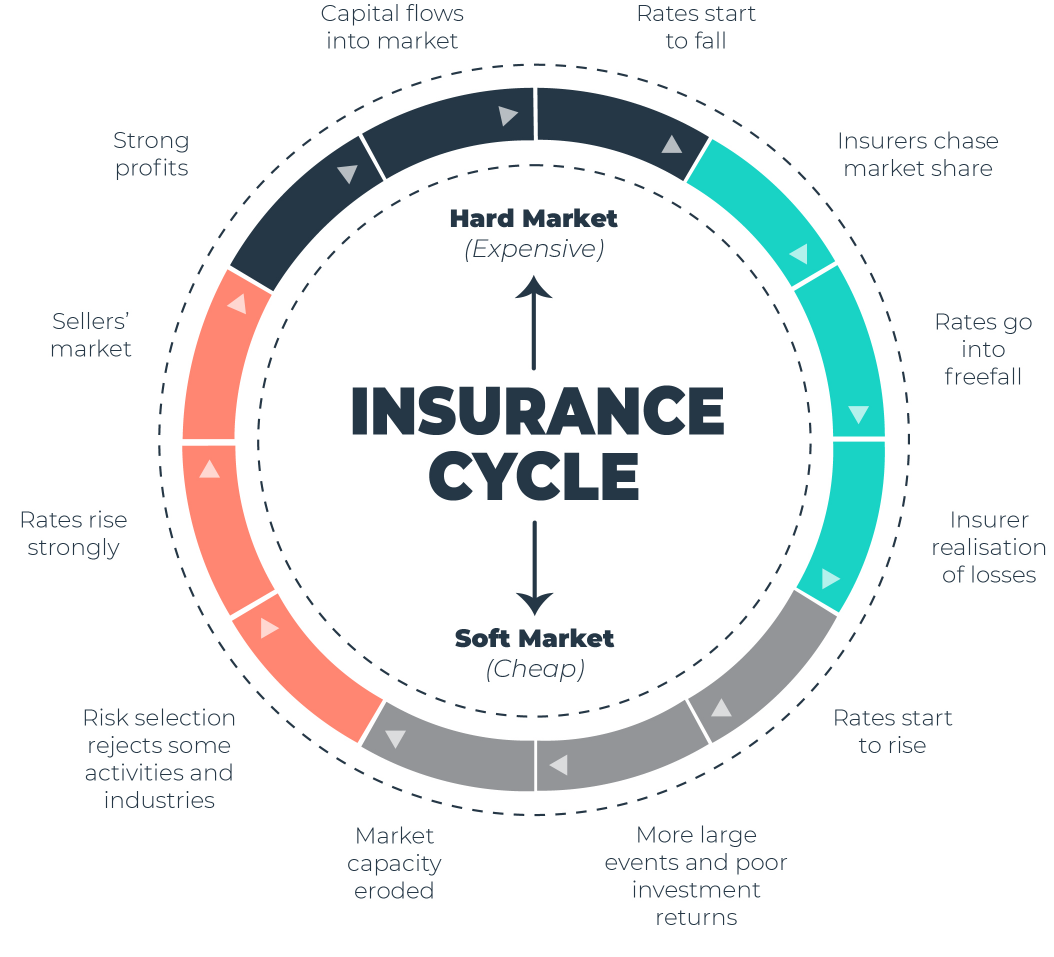

STATE OF THE MARKET UPDATE - A Hardening Insurance Market & Rising Premiums - June 2021

All industries experience cycles of expansion and contraction, and this is particularly true of the insurance industry. Although no two cycles are exactly the same, insurance industry cycles typically last between three to ten years and incorporate phases marked by an expansion (hard market) and a contraction (soft market) of insurance availability.

Today, Australia is well into a hardmarket across most insurance lines effecting the majority of industries.

The most recent Marsh ‘Global Insurance Market Index’ report found that Australia’s commercial insurance pricing increased 35% in the fourth quarter of 2020, while financial and professional lines rose a whopping 51%. Both lines have been continuing an upward trend that began in the first quarter of 2017.

This suggests that the insurance industry is currently hovering around 10-11 o’clock on the insurance clock pictured above, with insurance experts predicting that the hard market will continue into 2021/2022, further exacerbated by COVID-19 and other issues.

What is a soft market vs. a hard market?

In a soft market, insurance companies have a broader appetite for “risk”, greater underwriting flexibility, and compete with one another by (generally) lowering premiums to attract more customers.

This is a period of time when insurance companies have high-dollar reserves and can make money in the stock market. Thus, they can lower their premiums to a point where they either don’t make money or even lose money on the “underwriting” side of the equation.

The characteristics of a soft market typically include:

lower insurance premiums

broader coverage

relaxed underwriting criteria, which means underwriting is easier

increased capacity, meaning insurance carriers write more policies and higher limits

increased competition among insurance carriers

Alternatively, a hard market is when there is a high demand for insurance, but a lower supply of coverage available. The primary impact on customers is a rise in the price of insurance, and sometimes insurers reduce or stop providing cover for certain types of risk altogether.

The characteristics of a hardmarket typically include:

higher insurance premiums

low interest rates

an increase in the frequency or severity of losses

more stringent underwriting guidelines, making it more difficult to find options for insurance

fewer insurers writing certain coverage lines and specific industries

diminished capacity, meaning there are fewer insurers writing certain coverage lines and specific industries

less competition among insurance carriers

Why are we currently facing a hard market?

The last few years has seen Australia gradually move towards a hard market; however it was 2020 where we saw insurance profitability take the biggest hit.

2020 reported only $35m in profit for the calendar year, which was a staggering 98.9% decrease on the $3.1bn reported in 2019. This profit loss was largely driven by natural catastrophe claims costs, provisions for business interruption claims, a large strengthening of long-tail claims reserves (long-term, large payout settlements), and falls in investment income.

Below is a little more detail behind the key contributing factors that have played a role in Australia’s transition from a soft insurance market to a hard insurance market over the last few years.

Increases in the frequency or severity of losses (natural catastrophes)

The Australian market suffered heavy catastrophe losses in 2020, shaken by bushfires, cyclones, floods and hailstorms which raged across much of Australia’s eastern seaboard and resulted in immense financial costs for the insurance industry. Insurers that have paid large claims for certain risks may be reluctant or unwilling to insure those risks in the future

The 2019-2020 “Black Summer” bushfires alone were unprecedented in terms of scale and damage. The impact of the bushfires resulted in over 30,000 claims, resulting in insurers paying out a total of $2.4bn. This was the most expensive claims payout since the devastating floods and Cyclone Yasi hit QLD in 2011, with insurance losses totalling over $4.5bn.

Insurers that have paid large claims for certain risks may be reluctant or unwilling to insure those risks in the future

Falling investment returns for insurers

Investment income fell by almost 50% during the year due to lower returns in equities, fixed interest investments and indirect investments, particularly during the COVID-19 impacted March 2020 quarter.

The COVID-related global economic downturn has caused interest rates to hover near zero %, decimating the investment return income which insurers have traditionally relied upon as an integral source of profit.

COVID-19 has exacerbated and extended the hard market conditions with significant losses in Directors & Officers Liability (D&O), Employment Practices Liability Insurance (EPLI), Event Cancellation and other lines.

Social inflation

Social inflation is the societal trend towards increased litigation, plaintiff-friendly legal decisions, and larger jury awards – all of which put pressure on insurer performance.

The average number of securities class action claims lodged per year in Australia has risen by 300% since 2011. Big banks and financial services firms also continue to face a litigious 12 months as last year's Hayne royal commission hearings inspire regulators, consumers and shareholders to take them to court.

The surge in shareholder class actions has notably made its mark on the Directors and Officers Liability (D&O) insurance market. The future of the D&O market hangs in the balance as availability dwindles and costs surge for D&O insurance products.

Rising cost of reinsurance

Reinsurance is the insurance that insurance companies purchase to protect their bottom line. Recent times have seen the cost of reinsurance increasing due to the large number of catastrophe losses around the world.

Typically, the reinsurance market drives insurance pricing trends. If reinsurers increase their costs significantly, insurers react by passing down their primary premium to the consumer. It’s only natural that as one rises, so does the other.

Australian agreements on reinsurance pricing for the first half of 2020 saw increases in the range of 10% to 20%.

How to Survive a Hard Market

Here are some high-level recommendations you can adopt today to help you mitigate hard market impacts on your insurance spend.

1. Plan ahead

Stay ahead of your renewal process and communicate early with your broker to help you identify how you will be impacted by the increased cost of insurance.

2. Be prepared to provide more detail at the time of renewal

Due to increased underwriting scrutiny, you may be required to submit additional applications.

3. Partner with a specialised and trustworthy broker

With shrinking capacity, insurers will be scrutinising the number of brokers and wholesalers with whom they work. Be sure to work with a broker with strong insurer relationships and knowledge of your industry.

4. Don't wait until renewal to review your policies and procedures

Maintain communication with your broker during your policy period – not just during the renewal process – to understand where improvements can be made.

5. Update your integrated risk management programs and procedures

Be prepared to explain your claims and what measures you took to mitigate this exposure.

The bottom line

Even before the coronavirus crisis hit, the insurance industry was in a period of significant rate hardening.

Insurers are relying upon premium adequacy to cover losses and generate profits by increasing rates, refining their risk appetite, reducing the capacity they are willing to offer, sharpening their underwriting, and incorporating restrictive language in their policies.

This insurance trend is most likely to continue over the next two years, or even longer, so consumers should budget appropriately and work closely with their brokers to evaluate the efficacy of their risk management strategy.

The key is to take proactive steps now to save you in the future.

We’re here to help. If you’d like to get more advice on the current 'hard market' and how it might impact your business or insurance premiums, please contact us.

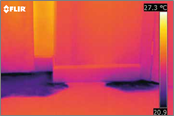

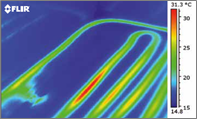

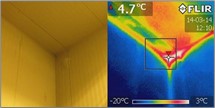

Thermal imaging can detect any problems areas in the workplace that are susceptible to temperature fluctuations – helping to prevent and manage things like electrical failure or electrical “hot spots”, excessive friction with machinery, moisture penetration or air leaks.

A thermal scan can reduce the likelihood of problems long before they arise, saving your business from considerable downtime and costly repairs.

It’s recommended that a thermal scan be conducted every 1 to 3 years (depending on the size and nature of your business).

Prevention is better than the cure.

What is thermal imaging and what are its benefits?

Thermal imaging – or thermography – is the process of using a specialised camera to measure infrared radiation emitted by an object regardless of lighting conditions. The varying levels of radiation are then converted into a unique colour gradient that relates to fluctuations in temperature, accurate to one-tenth of a degree.

As a non-invasive and visually concise tool, thermal imaging helps to uncover any potential problem areas in the workplace efficiently and safely. It’s an effective method of protecting your business’ assets, helping to prevent significant loss or damage to stock, equipment, or machinery, and can ensure the safety and security of your employees and your overall operation.

Thermography is used for a variety of purposes, and can return many benefits, like:

Measuring temperature variations and identifying target areas that need repair

Reducing outages and electrical energy costs

Reducing the risk of expensive equipment damage due to electrical fault

Locating electrical hot spots

Detecting air leaks and moisture penetration

Eliminating the need for exploratory demolition

Minimising long-term repair costs

Helping to control insurance claims costs

“22% of industrial fires are caused by faulty electrical equipment."

Using thermal imaging to reduce your insurance premiums.

Thermal imaging is becoming increasingly common for many Australian businesses to use as a way to decrease their commercial insurance premiums. Because of the value the technology can provide in preventative maintenance programs, insurance companies are rewarding businesses who are taking action to establish a low-risk environment and fire-reduction strategies. This consequently ends up providing access to lower insurance costs and prevents production downtime.

How often is thermal imaging needed?

There are no set standards – it will depend on the type of equipment your business uses, and the load the system is under.

As a guide, for a regular office building, a thermal imaging scan should be conducted every 2 to 3 years. For a manufacturing site – which has a high-power drain on the electrical systems – a scan at least once a year is advised.

The frequency of a thermal scan for your business can also be more accurately identified during a risk assessment of the premises, or at the request of your insurer or broker.

Below are some of the ‘higher risk’ sectors and environments where an annual thermal imaging scan can help to strengthen a business’s loss prevention program.

Electrical maintenance

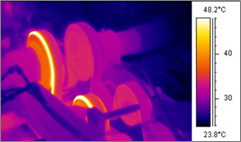

Thermal imaging can discover over-heated components in electrical devices and switchboards (preferably while under peak loading), accurately detecting hot spots generated from issues like:

Loose electrical connections

Unbalanced loads

Overloading of electrical circuits

Deteriorated electrical insulation

Damage caused by pests chewing on wires

These tests can help prevent serious injury, or even death from electrocution, while also saving your company time and money.

Construction

A thermal scan will help locate building defects such as missing or faulty thermal insulation, heat leaks, delaminating render, and any condensation problems. Results can be used to improve the efficiency of heating and air-conditioning units.

Plumbers

Use thermal imaging to inspect sites of possible leaks, mainly through walls and pipes. Since the devices can be used at a distance, they’re ideal for finding potential problems in equipment that is either hard to reach or might otherwise pose a safety issues to workers.

Cool rooms

Thermal imaging can be used in cool rooms, freezers, and temperature-controlled facilities to identify variances in temperature through vapour leakage or thermal transfer in the insulated panelling. Any fluctuations in temperature can impact product shelf life, not to mention greatly increase energy costs.

A scan is best performed at completion of a cool room construction. It will pinpoint the exact location of a possible thermal leak between panel and connection points.

Roofing

Most roof failures occur within the first seven years. Even if your roof is relatively young, a thermal scan can help reveal any accumulated moisture below the surface – moisture creates an environment conducive to mould.

Infrared inspections can detect issues on roof membranes, saving you the effort and the significant expense of dismantling and replacing the entire surface.

Mechanical equipment and machinery

Thermal imaging can also be used on mechanical equipment to detect issues like motor bearing problems or motor shaft misalignment. When operating under normal load conditions, thermal imaging scans on equipment and machinery can detect:

Excessive friction

Non-uniform heat flow

Temperature distributions

Motor and bearing wear

Pipe insulation

Tank levels

How much does a professional thermal imaging scan cost?

This will depend on the size and nature of your business. Most small commercial buildings can have their main switchboards and associated components inspected for under $500. For larger operations (e.g. a scan of multiple rooms, switchboards or equipment), you can expect a cost between $1,500 - $2,000.

Even though a good quality thermal camera can be purchased online for around $500 these days, getting a professional to perform an infrared inspection is much more involved than a simple ‘point and shoot’ approach.

A professional inspection is all about gathering accurate and reliable data, having it interpreted correctly, and then clearly communicating those findings to the business owner so that they can make reliable and informed decisions.

Keep in mind that there are regulations for certain industries that require their thermal imaging scan to be completed by someone with a Level 1 Certificate in Infrared Thermography. These industries include: electrical and mechanical, building, horticulture and agriculture, dairy, defence, and security.

Getting a regular professional thermal imaging scan of your business might seem expensive initially, but it’s a small price to pay if it means avoiding costly damage to your equipment, long-term repair costs, loss of production time, or even loss of your business altogether.

As the old adage goes, prevention is better than the cure.

If you'd like more information about using thermal imaging at your business, please get in touch.

Sources: flir.com.au

WHAT INSURANCE DO I NEED FOR MY LANDSCAPING BUSINESS?

All landscapers should carry public liability insurance. Similarly, landscape designers should carry professional indemnity insurance.

Public Liability

Public liability insurance protects you and your business in the event a customer, supplier or member of the public is injured or sustains property damage as a result of your negligent activities.

Professional Indemnity

Professional Indemnity insurance covers your legal costs and/or damages payable if something goes wrong with a landscaping project which leads to financial loss to your client. Examples include negligence leading to loss of plants, or failing to pass on instructions that lead to a mistake during construction. It's wise to take up professional indemnity insurance if you provide services or advice in a professional capacity.

Additional insurance considerations:For domestic projects larger than $16,000, you should also hold Domestic Building Insurance, which guarantees the structural components of the project for up to six years - just like warranty insurance when building a house. Unregistered landscapers cannot take up domestic building insurance.

Contract Works

Contract works insurance covers damage to the work you are doing while under construction from events such as flood, storm, theft of materials and fire. Although this type of cover is often insured by the builder on the project, there may be circumstances where this type of cover falls to you. To determine if this is required, we suggest you check your contract details.

WHAT DOES PUBLIC LIABILITY INSURANCE COVER?

All it takes for a claim to be made is a trip hazard created by your work activities or accidentally causing damage to your client’s property.

What you're typically covered for:

legals costs incurred for settlement of a claim

cover for others acting on your behalf when the incident occurred

loss or damage of goods

loss or damage of someone else's property

first aid expenses

injury to others while on the premises

HOW DO I COVER MY TOOLS AND EQUIPMENT?

Tools and equipment can be covered under a standard business insurance pack or a specific Tools Of Trade policy. Both can cover the replacement costs of your tools if they are stolen or damaged, however not all policies provide complete replacement due to depreciation. A broker will be able to advise on the most suitable option for you.

WILL MY LIABILITY COVER LEGAL EXPENSES IN THE EVENT OF A CLAIM?

Yes, this is an integral component of a public liability policy. You will be covered for costs awarded to the claimant if they bring a court case against you as a result, as well as cover for your defence costs, including legal expenses incurred in assessing or defending a claim.

ARE MY SUBCONTRACTORS COVERED BY MY POLICY?

No. If you work as a subcontractor, even if you only work for one employer or company, you're considered to be running your own small business and are therefore responsible for your own actions.

SHOULD I UPDATE MY BROKER OF CHANGES TO MY BUSINESS ACTIVITIES?

Small changes can make a big difference to your insurance, so it's important to update your broker or insurer whenever there's a significant change to your business. Things like a change of address, an increase in turnover, a company rebrand, or an increase in your level of cover could all have ramifications on your existing insurance cover.

To find out what type of cover is best for you and your business, contact us.

Minister for Agriculture, David Littleproud, has recently announced (Oct2020) grant applications are now open for Australian grape growers who were impacted by crop loss from the Black Summer fires of 2019-20.

Wine grape growers who suffered crop loss due to smoke taint in New South Wales, Victoria, South Australia, Tasmania and the Australian Capital Territory, but whose vineyards are outside of bushfire activated areas, can now access up to $10,000 to support their recovery efforts.

Further information on eligibility, contact numbers and links to the grant application for each state can be accessed via the National Bushfire Recovery Agency website and read details ongetting bushfire ready.

If you have any questions about the announcement, your eligibility for the grant, or the application process itself, please just drop us a line and we'd be happy to assist.

Working in the transport industry requires stamina, dedication, concentration, and can often be labour intensive. It's also not without its risks, such as being more vulnerable to road accidents, stress of adhering to stringent time pressures, working with dangerous goods and/or heavy materials, and the more common injuries of sprains, strains and musculoskeletal injuries.

Midland continues to work closely with the Transport Workers Union (TWU) as we endeavour to protect transport industry workers across Australia, which is why we have developed a market leading Personal Accident & Sickness Plan through our partner, AusInsure.

This comprehensive plan is designed specifically for transport operators and their employees, and provides exceptional coverage to ensure total protection should you fall sick or get injured on the job.

In addition, this policy now also covers AusInsure members who are diagnosed with COVID-19 (subject to waiting periods).

The BOM states there's now three times the normal likelihood of La Niña developing over spring/summer 2020, which typically means more rain and an increased chance of flooding and tropical cyclones.

Plan ahead – prepare your home and/or business so they’re protected from any potential extreme weather events.

Check your insurance policy to ensure you’re adequately covered - pay particular attention to your exposure to storm and flood events.

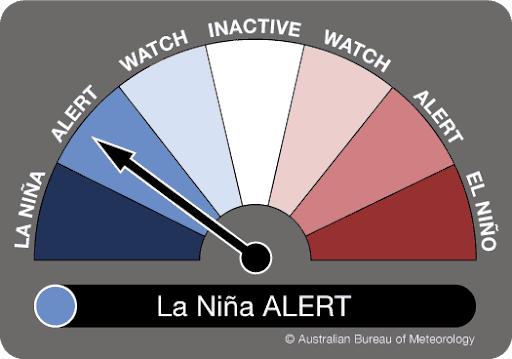

A La Nina ‘ALERT’ status has been issued by the Bureau of Meteorology for the first time since February 2018.

The outlook has recently increased to an ‘ALERT’ status from a previous ‘WATCH’ status, putting the chance of a La Nina in 2020 at 70% which is around three times its normal likelihood. This typically means we are likely to see more (and heavier) rainfall during this years’ spring and summer months, as well as an increased risk of flooding and tropical cyclones.

La Niña typically means:

Increased rainfall across much of Aus.

Cooler daytime temperatures (south)

Warmer overnight temperatures (north)

Shift in temperature extremes

Decreased frost risk

Greater tropical cyclone numbers

Earlier monsoon onset

With this increased risk in mind, homeowners and business owners across high risk regions need to place awareness and preparation as a top priority to help protect against a potential extreme weather event. See outlook maps here or below.

As the reality of climate change starts to really hit home, it’s no longer safe to make decisions on the basis that an extraordinary event is unlikely to happen.

“The BOM’s La Niña watch announcement is a great opportunity for brokers and customers to plan ahead and make sure we’re all prepared and ready if an extreme weather event does eventuate.”

Source: David Gow – QBE’s Head of Major Loss Property Claims

Below are a few preventative steps you can take to better protect your home and/or business in the case of a flood or cyclone event.

Your insurance policy:

Review your cover to make sure you have adequate insurance in place, especially your exposure to storm and flood as it may be excluded under standard wordings.

Assess your flood exposure.

Take a close look at your policy exclusions, especially flood.

Consider business interruption insurance – are you covered should you need to close your business?

Your home or business:

Get a building inspection and follow the recommendations.

Maintain roofs and guttering, and ensure your buildings are watertight. Reducing the likelihood of damage prior to inspection is important.

Place stock and electrical equipment above the recommended level to avoid water damage.

If you have a basement, install a submersible pump.

Check drainage on your property. Your council should also be keeping water channels clear.

Consult with your local council.

Physically prepare your home and business for severe weather.

Develop an evacuation plan for you, your employees and your family.

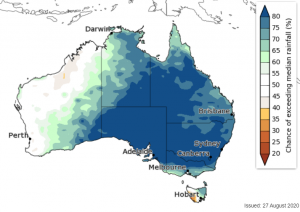

BOM Rainfall Outlook – the chance of above median rainfall for September to November 2020.

“It's about being prepared and understanding your exposure, whether that relates to a private residence, or a commercial or industrial occupancy”.

Below is a list of emergency services by state - they house information and resources to help you plan and take practical actions to protect your assets and understand the risks:

If you would like to chat with one of our specialist industry brokers for advice, to analyse your existing policy, or to gain a free assessment on the insurance coverage that is best for you, please just drop us a line.